Shifting Landscape

Change is often considered positive

but not necessarily so for the banking and financial sector. Any drastic event acts as a threat, as banks and financial institutions are the first to get impacted. The impact may include a rise in fraudulent activities such as an increase in fraudulent loans, higher delinquency rates, and impacting credit portfolios breaching normal risk appetite. If a bank is not adequately prepared, such changes can disrupt normal lending operations, damage its reputation, and even result in regulatory penalties.

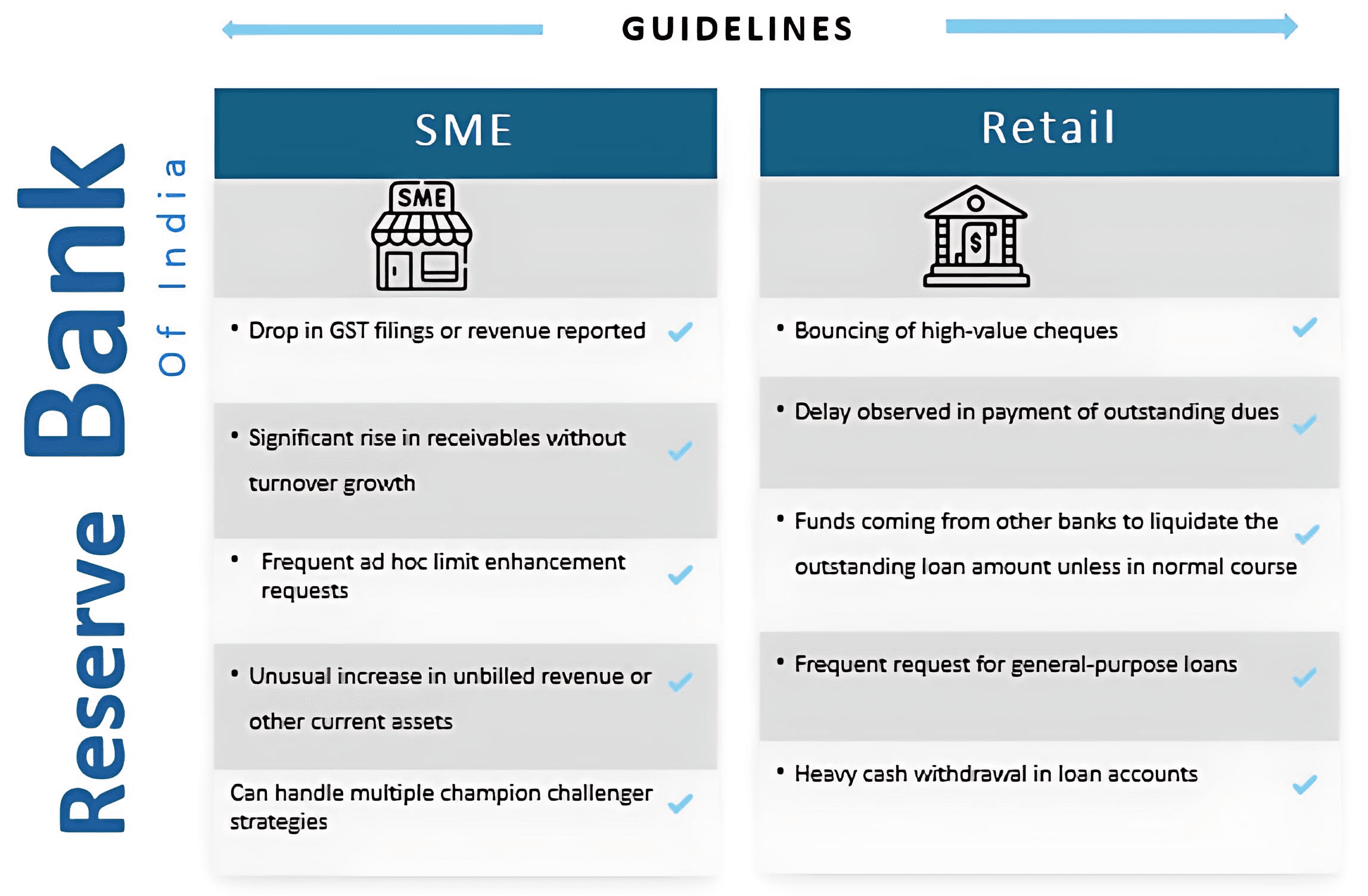

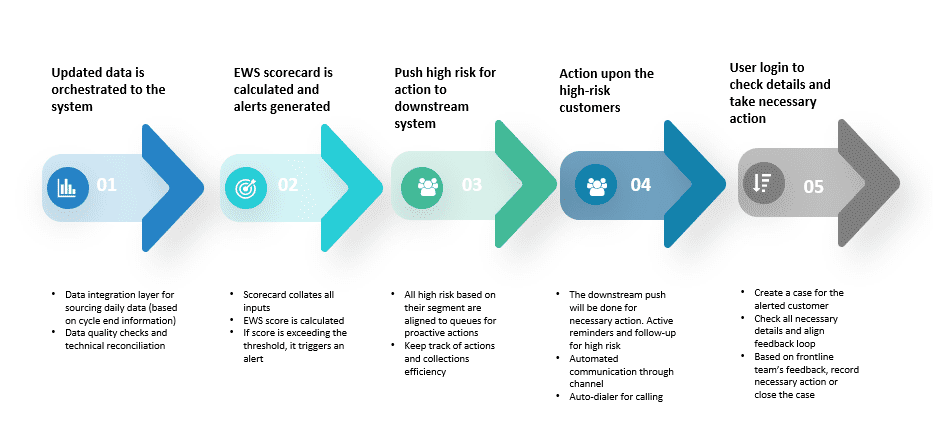

To mitigate such threats, RBI released Directions on Fraud Risk Management , introducing EWS framework to identify emerging risks before they escalate. EWS will allow BFSI to strengthen by minimizing the risk at the origination as well as identify potential RFA (Red Flagged accounts) during the account management stage, stretching internal controls and minimizing the incidences of fraud.

Leave A Comment